If you drive your car safely for an entire year and file absolutely zero claims, can your premium still increase at renewal? This is a common question people have. While a clean record is highly beneficial, keep in mind that your premium is not solely dependent on whether you made a claim in the following year. According to experts, a vehicle’s premium is typically calculated using a complex mix of variables, including its age, engine capacity, and specific coverage selections. “Consequently, several external and internal factors can push your premium upward, completely independent of your driving history,” said Aditya Kumar, Head, Motor Underwriting, Digit Insurance.

Most common cause behind a spike in premium

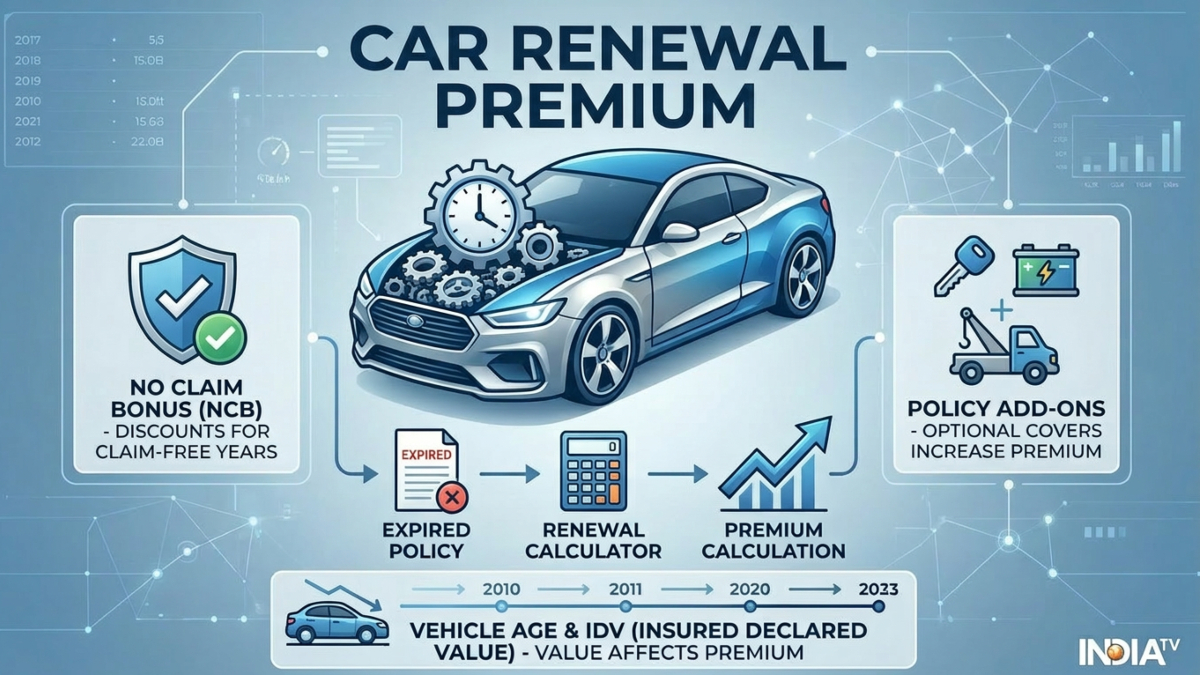

One of the most frequent causes of a premium spike is a lapsed policy. Allowing your insurance to expire, even for a short window, breaks your continuous coverage. Insurers may view this gap as a high-risk indicator, which may result in a marginal rate increase when you try to renew your policy.

“Furthermore, letting a policy lapse can put your hard-earned ‘No Claim Bonus’ or NCB at risk. This reward system operates on a tiered progression, starting at a 20 per cent discount after your first claim-free year and increasing to 25 per cent, 35 per cent, 45 per cent, and finally capping at 50 per cent after five consecutive years. If it lapses more than 90 days (grace period) of your renewal due date, the NCB can be set to nil, making you lose this cumulative discount instantly, thus inflating your renewal cost,” Kumar said.

What else can lead to a spike in premium?

Even if your policy remains active, the choices you make on the renewal form can also affect the premium. For instance, adjusting your Insured Declared Value (IDV) has a direct financial impact. Opting for a higher IDV to reflect a better market value for your car can lead to your premium rising.

Similarly, selecting additional add-ons you did not opt for in the previous year can increase your final premium. Generally, add-on premiums increase as the vehicle gets older. “In addition, the base Own Damage premium rate may also change at certain vehicle age milestones. For private cars, these rate revisions typically occur after 5 and 10 years of vehicle age,” he said.

Beyond your personal choices, macroeconomic changes may also play a role sometimes. The premium for Third-Party (TP) insurance is regulated and set by the IRDAI. If the regulator decides to revise and increase these standard baseline rates, your total premium may automatically go up, regardless of how safe a driver you are.

How to manage your insurance premium renewal cost?

You can strategically manage your renewal costs. First, evaluate your add-ons strictly, selecting only those that protect against risks you actively face. For older cars with declining market values or low IDVs, maintaining an expensive comprehensive cover might not make financial sense, especially if the annual premium outweighs the cost of minor self-funded repairs. Additionally, you can look into modern, flexible structures like a Pay As You Drive (PAYD) add-on.

“If you generally drive less, you can commit to a lower kilometre slab as low as 2,500 km, which can dramatically slash your premium, sometimes paying just 25 per cent to 40 per cent of a traditional policy’s original cost,” Kumar added. While expanding your kilometre limit will gradually increase the price, experts are of the view that it is still an effective, customisable way to keep your premiums low.

ALSO READ | NSE, SBI Mutual Funds IPOs push unlisted shares into focus: How to buy, tax rules and risks